Transfer of a Business as a Going Concern (TOGC): The Ultimate Singapore GST Guide

- Roger Pay

- Jun 6

- 8 min read

Transfer of Business as Going Concern

Transfer of a Business as a Going Concern (TOGC): The Ultimate Singapore GST Guide

Are you planning to sell or restructure your business in Singapore? If you are transferring an entire operating business—including its commercial properties, stock, and company vehicles—you might be looking at a massive Goods and Services Tax (GST) bill.

However, under Inland Revenue Authority of Singapore (IRAS) guidelines, if the transaction qualifies as a Transfer of a Business as a Going Concern (TOGC), it is treated as an excluded supply. This means 0% GST is charged on the transfer, protecting your cash flow and simplifying the transaction.

Here is everything you need to know to ensure your business transfer qualifies for TOGC benefits.

What is a Transfer of a Business as a Going Concern (TOGC)?

In Singapore, when you sell business assets individually, GST (currently 9%) normally applies to each taxable asset. However, a TOGC occurs when you transfer an entire operating business—or an independent, capable part of it—as a running function to a new owner.

Instead of just selling off "parts," you are handing over a fully operational machine that the buyer can immediately continue to run.

What Assets Can Be Included?

To qualify as a TOGC, the transfer typically encompasses all core operational assets, such as:

Operating Properties: Factories, warehouses, or retail spaces used for the business.

Book Stock: Raw materials, inventory, and work-in-progress goods.

Vehicles & Equipment: Delivery vans, machinery, and office hardware.

Intangibles: Goodwill, customer databases, and intellectual property.

The Big Benefit: Why TOGC Status Matters

The Bottom Line: Under IRAS rules, a qualified TOGC is treated as an excluded supply. Neither the buyer nor the seller needs to account for GST on the transfer of the properties, stock, or other business assets.

Without TOGC status, a $5 million business transfer could trigger an immediate $450,000 GST liability. While the buyer might eventually claw this back as input tax, the temporary cash flow strain and administrative hurdles can derail a deal. TOGC completely eliminates this friction.

IRAS Qualifying Conditions for TOGC

To enjoy the GST-excluded status, your transaction must strictly satisfy all of the following IRAS conditions:

Condition | What It Means |

|---|---|

1. Identifiable Business | The assets transferred must form a clearly identifiable, operational business (or a standalone part of it, like a specific branch). |

2. Carrying on the Business | The buyer must intend to carry on the same kind of business with the transferred assets. They cannot buy the business just to immediately liquidate the assets. |

3. No Interruption | The business must be a "going concern" at the time of transfer. There should be no significant break in operations before or after the handover. |

4. GST Registration Status | The buyer must already be a GST-registered person, or become GST-registered immediately as a result of the transfer. |

5. Continuity for Property | If commercial properties are involved, the buyer must continue using them for the business or take over existing tenancy agreements. |

Crucial Pitfalls to Avoid

Failing an IRAS audit on a TOGC can result in heavy penalties and back-dated GST liabilities. Watch out for these common mistakes:

Selling Assets, Not the Business: If you sell the machinery and vehicles but do not transfer the customer contracts or the ability to run the trade, IRAS will view it as a standard sale of assets, and GST will apply.

Buyer’s GST Status: Always verify that the buyer is GST-registered before the completion date. If they fail to register in time, the TOGC status is void.

Post-Transfer Changes: If the buyer completely changes the nature of the business immediately after taking over, IRAS may retroactively disqualify the TOGC.

Streamline Your Business Transfer

Navigating a TOGC requires precise contractual wording and a deep understanding of Singapore tax law. Ensuring that your Sale and Purchase Agreement (SPA) explicitly outlines the TOGC conditions protects both parties from unexpected tax liabilities.

Are you preparing for a business handover or restructure? Don't leave your GST obligations to chance. Speak to a qualified corporate tax professional today to review your business asset structure and secure your TOGC eligibility.

Frequently Asked Questions

Does TOGC apply to shares?

No. The sale of shares in a company is an exempt supply under Singapore GST law. TOGC specifically applies to the transfer of business assets as a running function.

Do we need to apply to IRAS for TOGC approval?

You do not need prior approval from IRAS to treat a transfer as a TOGC. However, both the seller and buyer must maintain proper documentation and satisfy all legal conditions, as IRAS routinely audits these transactions.

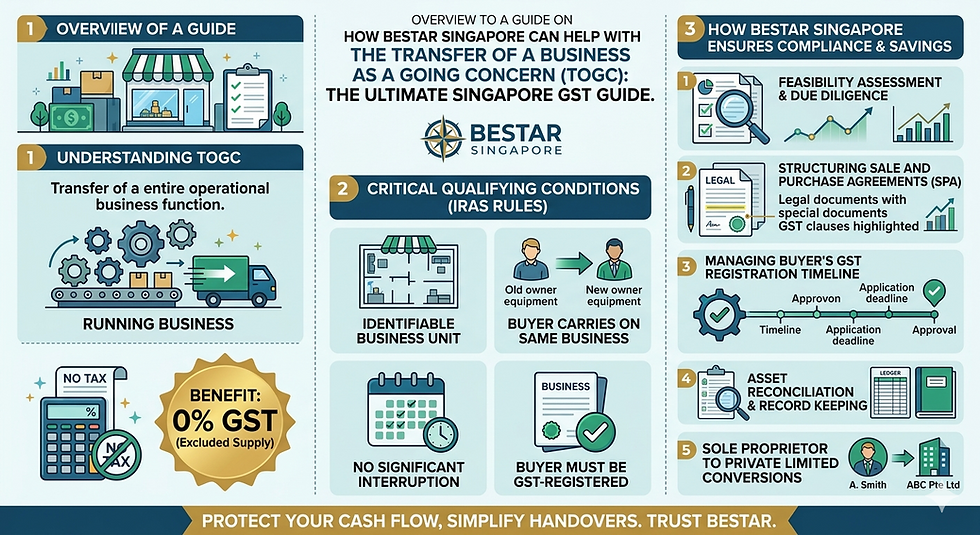

How Bestar Singapore Can Help with the Transfer of a Business as a Going Concern (TOGC)

Transfer of a Business as a Going Concern (TOGC): The Ultimate Singapore GST Guide

Are you planning a corporate restructure, converting a sole proprietorship to a private limited company, or executing a mergers and acquisitions (M&A) deal in Singapore?

When you transfer an entire operating business—including its commercial properties, inventory, and company vehicles—to a new owner as a running function, the transaction can trigger an immediate and massive Goods and Services Tax (GST) liability.

However, under Inland Revenue Authority of Singapore (IRAS) rules, a qualified Transfer of a Business as a Going Concern (TOGC) is treated as an excluded supply. This means 0% GST is charged on the transfer of the assets, preserving vital transaction cash flow.

Achieving this status requires absolute compliance with rigid tax criteria. Here is how partnering with Bestar Singapore ensures your business handover is seamless, compliant, and fully optimized for tax savings.

What is a TOGC and Why Do You Need Expert Guidance?

In a standard asset sale, a GST-registered business must charge the prevailing GST rate (currently 9%) on all taxable assets sold. In a multi-million dollar business transfer, paying 9% GST upfront on factory properties, book stock, and equipment can place an immense cash strain on the buyer—even if they can eventually claim it back as input tax months later.

Under the GST (Excluded Transactions) Order, a qualified TOGC is treated as outside the scope of GST.

The Core Challenge: IRAS does not require prior approval for a TOGC, but they heavily audit these transactions. A single misstep can result in IRAS retroactively disqualifying the TOGC status, leaving the seller liable for back-dated GST, heavy late-payment penalties, and interest charges.

The Essential IRAS Qualifying Conditions for TOGC

To secure an excluded supply status, your transaction must strictly satisfy all of the following conditions simultaneously:

IRAS Requirement | What Must Occur in Practice |

|---|---|

1. Genuine Business Transfer | It cannot be a mere sale of individual assets. The transfer must actively put the buyer in possession of an operational business unit capable of generating revenue. |

2. Identity of Business | The buyer must intend to carry on the same kind of business using the transferred assets, rather than liquidating them or fundamentally changing the trade. |

3. Independent Operation | If only a specific division or branch is being transferred, that part must be completely capable of operating independently. |

4. Seamless Continuity | The business must be a going concern at the handover date. There can be no operational closure immediately before or after, aside from brief, necessary transition breaks. |

5. GST Registration Sync | The buyer must already be a GST-registered person on the date of transfer, or become compulsorily GST-registered immediately as a result of the transfer. |

How Bestar Safeguards Your Business Transfer

Navigating corporate asset handovers involves a complex mix of accounting, legal wording, and corporate secretarial management. Bestar provides an end-to-end service suite to completely eliminate tax risks for both buyers and sellers.

1. Robust Pre-Transaction Due Diligence & Feasibility

We thoroughly evaluate the business structure, current asset registers, and transaction blueprints. Bestar determines definitively whether your proposed transaction satisfies the "going concern" definitions or if it risks being flagged as a standard, taxable asset disposal.

2. Safeguarding the Sale and Purchase Agreement (SPA)

The tax intent of a transaction must be explicitly mirrored in your legal paperwork. We work to structure critical GST protection clauses within your SPA, ensuring that:

Both parties warrant their compliance with TOGC conditions.

Adequate asset description and valuation reconciliation protocols are put in place.

Clear indemnity clauses protect the seller if the buyer unexpectedly changes the business nature post-transfer, voiding the TOGC status.

3. Managing Strict GST Registration Timelines

The buyer’s GST status is the most common single point of failure in a TOGC. If the buyer is not registered on the exact date of the transfer, the entire tax exclusion fails. Bestar’s corporate tax team assesses the buyer’s liability to register (whether via the retrospective or prospective $1 million turnover threshold rules) and manages accelerated voluntary or compulsory GST applications with IRAS ahead of schedule.

4. Seamless Constitution & Corporate Secretarial Management

If your TOGC stems from changing a business constitution—such as converting an aging partnership or sole proprietorship into a private limited company—our corporate secretarial team handles the entire framework. From incorporating the new entity to executing the transfer of commercial property titles, leases, employee contracts, and vehicle ownerships, we ensure zero operational friction.

5. Compulsory Asset Reconciliation & Record Keeping

IRAS requires both the transferor and transferee to maintain meticulous records providing a clear description and value of each asset or asset class transferred. Bestar constructs comprehensive asset closing and opening balances, perfectly reconciling pre- and post-transfer asset values to ensure total audit readiness.

Typical Pitfalls Bestar Helps You Avoid

The Voluntary Registration Trap: Buyers often assume they can register for GST leisurely after taking over. Bestar ensures applications are submitted early so registration is live on or before the completion date.

Incorrect Input Tax Claims: While the transfer itself is GST-free, professional legal and accounting fees incurred during a TOGC do carry GST. Bestar properly categorizes these transaction costs so that both buyers and sellers can legally claim this input tax back against general business overheads.

Mixed Property Supplies: If a commercial property includes residential quarters, the GST treatment changes. Bestar isolates the asset classes cleanly to prevent over- or under-accounting for tax.

Partner with Bestar Today

A successful business transfer should be a milestone of growth, not a source of unexpected tax liabilities and administrative gridlock. By choosing Bestar, you gain a dedicated team of tax professionals and corporate accountants who align every element of your transaction with Singapore’s strict regulatory framework.

Planning a business transfer or corporate restructure? Contact Bestar Singapore today to speak with a corporate tax advisor and ensure your business transfer qualifies flawlessly for TOGC tax exemptions.

Frequently Asked Questions

Does a TOGC apply if I sell my company's shares?

No. The sale of shares in a company is automatically classified as an exempt supply under Singapore GST law. A TOGC specifically applies when you are transferring the underlying operational business assets rather than equity.

What happens if IRAS rejects our TOGC treatment after an audit?

If IRAS determines the conditions weren't met, the transaction reverts to a standard taxable supply. The seller will be legally required to issue a retrospective tax invoice to the buyer and remit the 9% GST directly to IRAS, often alongside late-payment penalties.

Can a loss-making business qualify as a going concern?

Yes. A business does not need to be highly profitable to be a going concern; it simply needs to be actively operational, trading, and handed over as a functioning business unit capable of making continuous supplies.

To help structure your upcoming transaction:

Request a timeline for converting a sole proprietorship to a Pte Ltd under TOGC

Review sample GST clauses for an Asset Purchase Agreement

Take the Next Step with Bestar Singapore

Don't let unexpected tax liabilities or structural missteps compromise your business transition. Whether you are executing a high-stakes M&A transaction, restructuring your group companies, or converting a growing local business into a Private Limited entity, Bestar's tax and corporate secretarial specialists are here to safeguard your cash flow.

Schedule a Professional Consultation Today

Let our corporate tax team handle the complexities of your asset transfer, from rigorous IRAS compliance vetting to contract optimization.

🌐 Visit Our Website: www.bestar-sg.com

✉️ Email Us Directly: admin at bestar-asia.com

📞 Call Our Singapore Office: +65 6299 4730

📞 WhatsApp Us: +65 8836 4489

How would you like to proceed with your transition planning?

Get an onboarding checklist for Bestar's tax advisory services

Explore the costs and fees for a corporate restructure setup

Comments