The Definitive Compliance Guide to Singapore GST Registration Thresholds for Partially Exempt Financial Supplies (2026 Corporate Edition)

- Roger Pay

- Jun 1

- 12 min read

Singapore GST Registration For Financial Supplies

The Definitive Compliance Guide to Singapore GST Registration Thresholds for Partially Exempt Financial Supplies (2026 Corporate Edition)

Navigating Goods and Services Tax (GST) registration rules in Singapore becomes exceptionally intricate when your organization deals with financial services. Under the Inland Revenue Authority of Singapore (IRAS) guidelines, financial activities require careful navigation of exempt, zero-rated, and standard-rated classifications.

Corporate Services Singapore

For entities making "partially exempt financial supplies"—meaning your revenue mix comprises both taxable transactions (such as asset management advisory fees or brokerage commissions) and exempt items (such as interest from corporate loans, realized foreign exchange gains, or equity issue proceeds)—miscalculating your actual GST registration liability can trigger backdated assessments, hefty compounding late fees, and rigorous audits.

This comprehensive guide breaks down the core structural frameworks, numeric tests, and multi-layered recovery mechanisms needed to master your compliance requirements under the current 2026 Singapore tax regime.

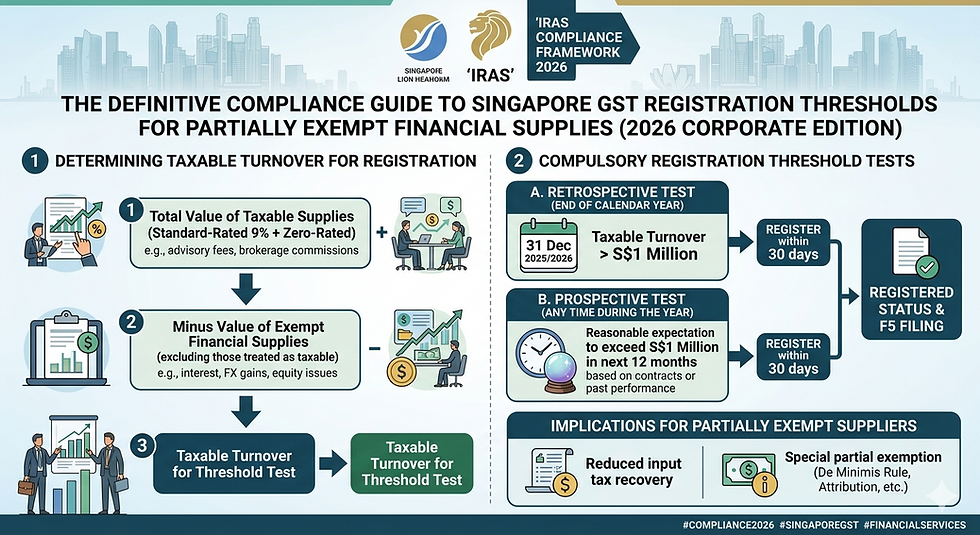

1. Core Statutory Foundations: What Counts as "Taxable Turnover"?

The fundamental trigger for compulsory GST registration in Singapore is crossing the SGD 1 million threshold. However, for a business generating complex financial revenue, the math is entirely unique. You do not simply add up your total corporate gross revenue. Instead, you must isolate what the Singapore GST Act categorizes as taxable turnover.

Taxable Turnover = Standard-Rated Supplies (9%) + Zero-Rated Supplies (0%)

Crucially, exempt supplies and out-of-scope transactions are completely excluded from this baseline calculation.

Supply Category | Prevailing GST Rate | Impact on Input Tax Recovery | Inclusion in SGD 1M Registration Threshold? |

Standard-Rated | 9% (Current 2026 rate) | Fully Claimable | Yes |

Zero-Rated | 0% | Fully Claimable | Yes |

Exempt | N/A | Non-Claimable (Subject to exceptions) | No |

Out-of-Scope | N/A | Non-Claimable | No |

Explaining the Financial Supply Classifications

To accurately track your threshold, you must break down every transaction stream according to its exact legal treatment under the Fourth Schedule to the GST Act:

Exempt Financial Supplies (Fourth Schedule, Part I): This covers core financial intermediation where identifying direct added value is structurally difficult. Examples include interest received from bank deposits or corporate loans, realized gains on foreign exchange transactions, the issue or transfer of equity securities/bonds, and the execution of derivatives contract strategies that do not involve physical product delivery.

Standard-Rated Financial Supplies (9%): Explicit operational charges, transaction management service fees, processing commissions, and advisory charges provided to local clients are fully taxable. If you run a corporate finance consultancy and charge a local client SGD 150,000 for structuring an M&A deal, that full amount is standard-rated and counts directly toward your registration threshold.

IRAS

Zero-Rated Financial Supplies (0%): Under Section 21(3) of the GST Act, if you supply those exact same financial advisory, underwriting, or arrangement services to a customer who belongs outside Singapore, the supply becomes zero-rated. Even though the tax rate is 0%, zero-rated transactions are legally taxable supplies. Therefore, they count toward your SGD 1 million registration limit.

2. The Compulsory Registration Framework: Two Distinct Legal Tests

IRAS enforces two strict legal tests to evaluate whether an entity must register for GST. If your business crosses the threshold under either test, you must submit your application within specified windows or face strict retroactive penalties.

+-----------------------------------------+

| Is Taxable Turnover > SGD 1 Million? |

+-----------------------------------------+

|

+-------------------+-------------------+

| |

v v

[ Retrospective Test ] [ Prospective Test ]

Evaluates historical performance Evaluates forward-looking data

at the end of a calendar year. on a rolling 12-month basis.

Test A: The Retrospective Basis

\The retrospective test evaluates historical performance at the conclusion of a specific interval. You must assess your historical figures at the end of every calendar year (31 December).

The Trigger: Your total taxable turnover (Standard-Rated + Zero-Rated supplies) for the immediate calendar year (1 January to 31 December) exceeds SGD 1,000,000.

Compliance Window: You are legally required to file a GST registration application with IRAS within 30 days (by 30 January of the subsequent year).

Effective Date of Registration: Your business officially joins the GST registry on 1 March of that next year.

Retrospective Exemption Caveat: If your taxable turnover crossed SGD 1 million at the close of the calendar year, you can apply for an exemption from compulsory registration only if you are absolutely certain your projected taxable turnover for the upcoming 12 months will not exceed SGD 1 million due to definitive, documentable business adjustments (e.g., structural corporate downsizing or the formal termination of a major revenue contract).

Test B: The Prospective Basis

The prospective test evaluates forward-looking data. This test operates on a rolling format rather than waiting for the calendar year to end.

The Trigger: At any given date, you can reasonably anticipate that your taxable turnover will surpass SGD 1,000,000 within the next 12 months. This anticipation cannot be mere optimism; it must be backed by concrete, verifiable business evidence.

VJM Global

Acceptable Evidence Standards: Signed service contracts, formally accepted customer tenders, fixed monthly retainer agreements, or highly structured historical financial trend lines demonstrating sudden volume escalations.

IRAS

Compliance Window: You must submit your registration application within 30 days of forming that forecast.

IRAS

Effective Date of Registration: For forward-looking projections, the effective registration date lands exactly two months from the forecast date (offering a streamlined onboarding runway).

VJM Global

3. Partially Exempt Financial Dynamics: The Critical Interplay

When an entity generates both taxable and exempt financial supplies, it is legally designated as a partially exempt business. This hybrid revenue status does not change the core SGD 1 million threshold rules, but it adds complex layers of data monitoring requirements.

Why "Incidental" Financial Revenue Trips Up Corporate Teams

Many non-banking commercial enterprises assume they are completely safe from these considerations. However, simple actions like parking spare operational cash in interest-bearing corporate accounts or engaging in routine treasury foreign exchange hedging create exempt financial supplies.

Thankfully, IRAS provides an operational carve-out known as Incidental Exempt Supplies. If your financial activities are merely secondary to your main commercial trade (e.g., earning bank deposit interest while running a software firm), those specific exempt revenues do not alter your clean status as a fully taxable business, and they do not complicate your base threshold tracking.

However, if your primary commercial operations rely on generating ongoing financial returns (such as a venture capital vehicle, a micro-lending office, or a proprietary algorithmic trading fund), you are officially operating a partially exempt structure.

The Immediate Consequence: Input Tax Strands

Once a partially exempt business formally registers for GST, its input tax recovery becomes highly restricted. While a standard business reclaims virtually all GST paid on business expenses, a partially exempt financial enterprise must run every dollar of incoming tax through a strict attribution funnel:

Claimable Input Tax = Direct Taxable Input Tax + (Residual Input Tax × Taxable Supplies / Total Supplies )

4. Operational Relief Systems: De Minimis Rule & Special Provisions

Because parsing every line-item expense creates a heavy administrative burden, the Singapore tax framework offers distinct relief mechanisms designed to simplify compliance and safeguard capital efficiency.

The De Minimis Rule: The Ultimate Safe Harbor

The De Minimis Rule functions as an operational exemption. It allows a registered, partially exempt business to claim 100% of its incurred input tax—including tax directly tied to making exempt financial supplies—provided its exempt activities remain safely under two specific thresholds.

To pass the De Minimis test, your business must satisfy both conditions simultaneously:

The Absolute Average Cap: The total value of all your exempt supplies does not exceed an average of SGD 40,000 per month across the designated accounting period (which equates to SGD 120,000 per quarter).

The Relative Revenue Proportionality Cap: The total value of your exempt supplies does not exceed 5% of the total value of all taxable and exempt supplies combined across that same period.

If your financial enterprise satisfies both parameters, the operational distinction between taxable and exempt inputs drops away for that period, allowing you to reclaim your input GST in full.

Special Remission Regimes for Qualifying Funds

For Singapore's asset management sector, strict adherence to partial exemption restrictions could unintentionally lower investment returns. To maintain the jurisdiction’s competitive edge as a premier global wealth hub, the government offers a specialized GST Remission for Qualifying Funds (currently extended through 31 December 2029).

Under this framework, investment funds that use prescribed local fund management firms and satisfy specific Income Tax concessions do not have to manage complex partial exemption attribution splits. Instead, they file a quarterly Statement of Claims to recover their incurred input GST at a fixed, industry-wide recovery rate (which typically sits between 85% to 90% based on annual adjustments).

5. Strategic Execution Blueprint: Achieving Compliance

For financial institutions and high-growth commercial entities approaching registration territory, ensuring compliance requires a structured, proactive plan.

1 Establish a Dual-Track Revenue Monitoring System

Continuous Monthly Process

Configure your enterprise resource planning (ERP) systems to log revenue streams under distinct tax category codes. Track your monthly rolling standard-rated and zero-rated sales lines together to monitor the SGD 1 million threshold, while isolating exempt financial streams in a separate sub-ledger.

2 Conduct Periodic De Minimis Pre-Screening Reviews

Every Quarter

Before closing out internal financial reporting periods, run your data through the De Minimis test. Check if your exempt revenue stays under SGD 40,000 per month on average and remains below 5% of total revenue. If you routinely cross either limit, prepare your workflows for partial exemption input tax apportionment models.

3 Execute Mandatory Digitalization and Onboarding Protocols

Within 30 Days of Crossing Threshold

Once you cross the threshold under either the retrospective or prospective test, complete the mandatory IRAS e-Learning course ("Overview of GST"). Note that for new voluntary registrations, you must transmit your transaction records using an approved InvoiceNow (Peppol-compatible) electronic invoicing platform.

4 Implement the Section 21(3) Zero-Rating Framework

Post-Registration Operational Launch

Once your registration is active, ensure your billing teams collect and store valid international residency evidence (such as overseas corporate business profiles or foreign regulatory tax certificates) for any overseas clients. This documentation is vital to defend your 0% zero-rated billing claims during an IRAS audit.

6. Real-World Case Studies: Threshold Math in Action

The following scenarios illustrate how these rules apply to different business models.

Case Study 1: The Boutique Quantitative Hedge Fund

A quantitative trading fund based in Downtown Core, Singapore, reviews its performance metrics to determine if it needs to register for GST.

[Fund Gross Revenue: SGD 4,500,000]

├── Exempt (Proprietary FX Gains): SGD 3,800,000

└── Taxable (Local Financial Advisory Fees): SGD 700,000

The Analysis: Even though the fund’s total gross intake of SGD 4.5 million is well above the headline threshold, its true taxable turnover is only SGD 700,000. Because the SGD 3.8 million in realized foreign exchange gains is classified as an exempt financial supply, it is completely excluded from the calculation.

The Compliance Outcome: Compulsory GST registration is not triggered. The fund can continue operating without registering, though it should review its revenue mix monthly to ensure its advisory fees do not cross the SGD 1 million line.

Case Study 2: The Cross-Border Fintech Payment Platform

A fintech startup provides API payment infrastructure and multi-currency transaction services to businesses across Southeast Asia.

[Fintech Revenue Baseline: SGD 1,300,000]

├── Zero-Rated (Infrastructure Advisory to Foreign B2B Clients): SGD 1,150,000

└── Exempt (Currency Exchange Spreads from Local Retail Users): SGD 150,000

The Analysis: The company's exempt currency spreads (SGD 150,000) are excluded from the registration check. However, its international infrastructure advisory services (SGD 1,150,000) are classified as zero-rated supplies under Section 21(3). Because zero-rated supplies are legally taxable supplies, they count toward the calculation.

VJM Global

The Compliance Outcome: The firm's taxable turnover stands at SGD 1,150,000, crossing the compulsory threshold. The company must apply for GST registration within 30 days of the trigger date, implement the InvoiceNow network framework, and file quarterly GST returns.

7. Crucial Compliance Penalties and Risk Management

Failing to register for GST on time can seriously disrupt a company's financial operations. If your business crosses the threshold and applies late, IRAS can retroactively apply your effective registration date back to the exact day your application was legally due.

Late Registration -> Retroactive Effective Date -> Out-of-Pocket GST Liability

This means your business becomes legally responsible for paying a flat 9% GST on all taxable sales made during that past unregistered period—even though you never collected that tax from your clients. On top of that backdated tax liability, IRAS can impose late-notification penalties of up to 10% of the total backdated tax due, along with extra compounding monthly fines.

For organizations dealing with partially exempt financial supplies, maintaining precise transaction tracking and running routine internal health checks is essential to ensure you stay fully compliant with the law.

To tailor these financial frameworks to your specific business model:

Analyze my specific financial revenue streams

Draft an internal IRAS input tax apportionment policy

Scaling Beyond Automated Platforms: The Strategic Corporate Governance and Financial Guide to Bestar Singapore

The Definitive Compliance Guide to Singapore GST Registration Thresholds for Partially Exempt Financial Supplies (2026 Corporate Edition)

For growing enterprises, mid-market businesses, and multinational subsidiaries operating in Singapore, compliance is not a static checkbox. Singapore's regulatory environment—governed by the Accounting and Corporate Regulatory Authority (ACRA) and the Inland Revenue Authority of Singapore (IRAS)—demands high-level technical oversight.

While automated, software-only platforms handle basic bookkeeping entry well, expanding organizations regularly hit structural friction points. When your business encounters multi-tiered corporate tax structures, cross-border Goods and Services Tax (GST) applications, statutory financial audits, or complex mergers and acquisitions (M&A), reliance on general tech support tickets introduces unacceptable compliance risks.

Bestar Singapore bridges this critical operational gap. Combining a sophisticated, cloud-integrated digital infrastructure with dedicated, partner-led professional expertise, Bestar provides an institutional-grade suite of accounting, auditing, taxation, corporate secretarial, and transaction advisory services across Singapore, Malaysia, and Hong Kong.

1. The Core Ecosystem: Full-Spectrum Corporate Infrastructure

Operating as a multi-disciplinary professional services firm, Bestar eliminates the need to coordinate with multiple boutique vendors. This comprehensive service footprint ensures that data flows seamlessly from corporate secretarial setups directly into year-end financial statement compilations and tax filings.

+-----------------------------------------+

| BESTAR SINGAPORE ECOSYSTEM |

+-----------------------------------------+

|

+------------------+------------+------------+------------------+

| | | |

v v v v

[ Corporate Sec ] [ Audit & Assurance ] [ Tax Advisory ] [ M&A Strategy ]

ACRA Governance Full Ledger Analytics IRAS Optimization Gold House M&A

Corporate Secretarial & Statutory Governance

Under Section 171 of the Singapore Companies Act, every private limited company must appoint a qualified corporate secretary within six months of incorporation. Bestar manages this entire legal mandate, ensuring total compliance with ACRA regulations:

Entity Onboarding & Structuring: Execution of local private limited incorporations, foreign branch registrations, and representative office formations.

Fiduciary Management: Provision of registered office addresses and resident nominee director services to satisfy statutory residency requirements.

Board & Shareholder Maintenance: Comprehensive management of statutory registers, preparation of board resolutions, drafting of meeting minutes, and execution of mandatory Annual Return filings.

Digital-First Accounting & Bookkeeping

Moving away from disconnected manual entry, Bestar integrates directly with leading cloud-based accounting platforms (such as Xero and QuickBooks Online) alongside Singapore’s national e-invoicing network, InvoiceNow. This modern integration syncs day-to-day transactions automatically, reducing traditional year-end data collection cycles by up to 30%.

2. Advanced Audit & Assurance: Full-Population Analytics

Traditional audit firms often rely on random sampling—reviewing a tiny percentage of transactions and extrapolating accuracy across the ledger. Bestar completely changes this model by integrating advanced data analytics to execute 100% population testing across your entire accounting ledger.

Feature / Metric | Traditional Audit Vendors | Bestar Analytics-Driven Framework |

Testing Scope | Random Statistical Sampling | 100% Ledger Population Testing |

Platform Integration | Manual Paper Trails / CSV Exports | Direct API Cloud Mapping (Xero, QuickBooks) |

Turnaround Time | Variable (Often 60 to 90+ Days) | Strict 30-Day Audit Guarantee |

Filing Formats | Basic Financial Statements | Full-Spectrum XBRL Compilation & Lodgment |

The 30-Day Onboarding and Audit Execution Workflow

Bestar eliminates the common delays associated with financial audits through a structured, transparent timeline:

1 Professional Clearance & Discovery

Days 1–3

Bestar manages the incoming transition entirely behind the scenes, securing professional clearance from your previous auditor and extracting historical accounting ledgers with zero operational downtime.

2 Cloud Data Syncing & Ledger Mapping

Days 4–7

Our specialized technology team links your data pipelines into our analytics systems, preemptively reviewing transactions for classification anomalies before field testing begins.

3 Substantive Analytics & Comprehensive Testing

Days 8–21

Chartered Accountants execute thorough data verification across your balance sheet. Queries are managed through a centralized platform, ending messy email chains.

4 Sign-Off, XBRL Compilation, & ACRA Submission

Days 22–30

Our team issues the final independent auditor’s report, converts your financial statements into full-spectrum XBRL formatting, and completes your mandatory ACRA lodgments.

3. Strategic Taxation and GST Compliance Solutions

Singapore’s tax landscape is highly rewarding but structurally precise. With a flat corporate tax rate of 17%, maximizing legitimate tax incentives requires proactive, ongoing planning.

Corporate Tax Optimization & Incentive Capture

Bestar’s tax advisors structure corporate filings to leverage Singapore's core tax incentives, including the Partial Tax Exemption (PTE) and the Three-Year Tax Exemption Scheme for New Start-Up Companies. Our team maps qualified expenditure lines to capture valuable Research and Development (R&D) tax incentives and productivity grants, ensuring your business preserves capital for expansion.

Goods and Services Tax (GST) Advisory

As businesses expand, tracking the compulsory SGD 1 million GST registration threshold becomes a critical operational requirement. This is especially true for firms dealing with complex international transactions or partially exempt financial supplies.

Taxable Turnover Checked for GST Liability = Standard-Rated Supplies (9%) + Zero-Rated Supplies (0%) - Exempt Financial Supplies

Bestar manages your entire GST workflow—from analyzing complex registration triggers on cross-border transactions under Section 21(3), to calculating input tax recovery under strict partial exemption rules, to submitting accurate quarterly F5 returns to IRAS.

4. Corporate Finance, Valuation, and M&A Advisory

When businesses reach market maturity, growth often requires strategic capital restructuring, divestments, or corporate acquisitions. Through its specialized divisions and strategic alignment with Gold House M&A, Bestar provides comprehensive transaction support to mid-market enterprises.

The Interdisciplinary Advantage: Successful M&A deals require more than just finding a buyer or seller. By keeping your accounting, legal governance, and transaction advisory under a single corporate umbrella, Bestar ensures that financial forensics, corporate valuations, and tax restructuring happen simultaneously.

Key Transaction Services

Comprehensive Due Diligence: Rigorous forensic investigations of target financial ledgers to discover hidden liabilities, evaluate working capital trends, and confirm true historical earnings.

Independent Business Valuations: Utilizing robust discounted cash flow (DCF), market multiple, and asset-based valuation models to establish a defensible corporate market value.

Deal Structuring: Structuring cross-border asset or share purchases to minimize retroactive tax exposures and maximize post-acquisition capital efficiency.

Bestar Asia

5. Transitioning with Confidence: The Bestar Advantage

Switching from a software-only accounting platform or a fragmented mix of boutique vendors to an integrated firm should never be a stressful operational burden. Bestar removes this friction with an explicit service-level commitment.

A Customer-First Pricing Model

Bestar believes that premium, partner-led accounting and audit services should remain accessible to growing mid-market enterprises. As a core corporate policy, Bestar actively reviews and matches lower fee quotes from alternative professional service providers while ensuring your business benefits from senior, chartered-level technical oversight.

Seamless Handover Framework

Our dedicated onboarding team handles the entire migration process for you. We coordinate directly with your outgoing service providers to securely transfer all accounting ledgers, historical tax returns, and statutory corporate registers. Your internal team can remain completely focused on everyday business growth, with no disruption to daily operations.

To optimize your corporate compliance structure and review your current overhead costs:

Comments