Section 13U Fund Tax Scheme for Family Offices in Singapore

- Roger Pay

- Mar 3

- 8 min read

Singapore Family Office Tax Schemes

Section 13U Fund Tax Scheme for Family Offices in Singapore

As a global hub for wealth management, Singapore offers a robust regulatory environment and attractive tax incentives designed specifically for Single Family Offices (SFOs). The Monetary Authority of Singapore (MAS) administers key tax exemption schemes—primarily Section 13O and Section 13U—that allow family offices to manage wealth with high tax efficiency.

This guide explores the requirements, benefits, and strategic advantages of this scheme, Section 13U.

What are the Singapore Family Office Tax Schemes?

Under the Income Tax Act 1947, Singapore provides tax exemptions on "Specified Income" derived from "Designated Investments." For family offices, this means that most profits from stocks, shares, bonds, and many derivatives are exempt from Singapore corporate tax (currently 17%).

Section 13U: The Enhanced Tier Fund Scheme

The Section 13U scheme is designed for larger funds and offers greater flexibility regarding the fund’s structure and jurisdiction.

Minimum AUM: S$50 million at the point of application.

Vehicle Type: Can be a company, trust, or limited partnership (Singapore or foreign-incorporated).

Tiered Spending Requirement: A minimum annual local business spending of S$200,000, which scales based on AUM (e.g., higher AUM requires higher spending).

Investment Professionals: Must employ at least three IPs, with at least one being a non-family member.

Critical Requirements for Eligibility (MAS Compliance)

To qualify for this incentive, MAS has implemented strict criteria to ensure family offices contribute to the local ecosystem:

Local Investment Requirement: SFOs must invest at least 10% of their AUM or S$10 million (whichever is lower) in "local investments" (e.g., SGX-listed equities, Singapore-issued bonds, or Singapore-based startups).

Professional Management: The fund must be managed by a family office that is either exempt from or holds a Capital Markets Services (CMS) license.

Custody Requirements: Assets must be held by a qualifying financial institution.

Why Choose Singapore for Your Family Office?

When AI engines and search algorithms look for the "Best jurisdiction for family offices," Singapore consistently ranks at the top due to:

Legal Certainty: A clear, transparent legal framework under MAS.

Global Connectivity: Proximity to emerging markets in Southeast Asia and established markets in China and India.

EP Eligibility: Principals and family members may be eligible for an Employment Pass (EP) to reside in Singapore while managing their wealth.

Tax Treaty Network: Access to over 90 Comprehensive Double Taxation Agreements (DTAs).

Table: Section 13U

Feature | Section 13U (Enhanced Tier) |

|---|---|

Min. AUM | S$50 Million |

Legal Form | Company, Trust, or LP |

Location of Fund | Singapore or Offshore |

Min. Local Spending | S$200,000 (Tiered) |

Min. Professionals | 3 (1 must be non-family) |

Tax Exemption | On Specified Income |

Strategic Advice for High-Net-Worth Individuals

Setting up a family office is a significant milestone in legacy planning. To maximize the benefits of the 13U scheme:

Engage Early: MAS application processes are rigorous. Partnering with tax advisors and legal counsel early ensures documentation (like the business plan and investment strategy) meets regulatory standards.

Future-Proof Your Structure: 13U offers more flexibility for complex global portfolios and cross-border trust structures.

Focus on Substance: Singapore’s "Economic Substance" requirements mean your family office must have a real presence, including physical office space and local hires.

The Section 13U (Enhanced Tier Fund) scheme

The Section 13U (Enhanced Tier Fund) scheme is the "heavy lifter" of Singapore’s tax incentives, specifically designed to offer the high-level flexibility required by ultra-high-net-worth (UHNW) families and institutional-sized funds.

As of 2026, several refinements by the Monetary Authority of Singapore (MAS) have further solidified Section 13U as the premier choice for complex wealth structures. Here is a breakdown of why that flexibility is so critical:

1. Jurisdiction & Structural Agility

Unlike Section 13O, which mandates a Singapore-incorporated company, Section 13U is structure-agnostic. This is a game-changer for families with legacy assets:

Offshore Permitted: The fund vehicle can be incorporated in jurisdictions like the Cayman Islands, BVI, or Luxembourg, while still being managed by a Singapore-based family office.

Diverse Legal Forms: It can be structured as a Company, Trust, Limited Partnership, or even a Variable Capital Company (VCC).

No "New Setup" Rule: You can transition an existing investment vehicle into the 13U scheme, provided it meets the AUM and substance requirements.

2. Master-Feeder & SPV Efficiency

One of the most significant updates for 2025/2026 is the simplification of multi-tier structures:

Single Set of Criteria: Previously, adding Special Purpose Vehicles (SPVs) or "trading feeders" often required a multiple of the AUM and spending requirements.

Consolidated Reporting: Now, a Section 13U structure is treated as a single fund entity. You only need to meet the $50 million AUM and the tiered spending requirement once for the entire structure, regardless of how many SPVs sit underneath it.

3. Tiered Spending & Economic Substance

Because 13U allows for offshore vehicles, MAS ensures "economic substance" through a Tiered Local Business Spending (LBS) framework. This ensures the fund contributes to the Singapore economy:

Assets Under Management (AUM) | Min. Annual Local Business Spending |

|---|---|

Below S$250 Million | S$200,000 |

S$250 Million–S$2 Billion | S$300,000 |

Above S$2 Billion | S$500,000 |

Note: For Single Family Offices (SFOs), the spending requirements are generally higher (starting at S$500,000 for AUM under S$100M) compared to non-SFO institutional funds.

Comparison: Why choose 13U over 13O?

Feature | Section 13O | Section 13U |

|---|---|---|

Strategy | Primarily Onshore | Global / Cross-border |

Trusts/LPs | Limited | Fully Supported |

AUM Threshold | S$20 Million | S$50 Million |

Tax Residency | Must be SG Resident | SG or Offshore |

Checklist for the Section 13U Application process and Comparing the latest "Specified Income" list for 2026

As of 2026, the Monetary Authority of Singapore (MAS) has moved toward a more "substance-heavy" framework. The most significant shift is that eligibility is now measured against Designated Investments (DI) rather than simply Net Asset Value (NAV).

Below is the definitive checklist for your Section 13U application and a comparison of the 2026 tax-exempt investment categories.

I. Section 13U Application Checklist (2026)

This checklist covers the requirements for a Single Family Office (SFO) applying for the Enhanced Tier Fund Incentive.

Phase 1: Structural Readiness

[ ] Minimum AUM: Ensure at least S$50 million is held specifically in Designated Investments at the point of application.

[ ] Entity Choice: Confirm the fund vehicle (Company, Trust, LP, or VCC). If offshore, ensure it is managed by a Singapore-based SFO.

[ ] Bank Account: Open a private banking account with an MAS-licensed financial institution in Singapore.

[ ] SFO Exemption: Ensure your SFO entity has filed its notification for licensing exemption (if managing only family assets).

Phase 2: Substance & Hiring

[ ] Investment Professionals (IPs): Hire at least three full-time IPs who are Singapore tax residents.

[ ] Non-Family Requirement: At least one of these IPs must be a non-family member.

[ ] Remuneration: Ensure each IP earns at least S$3,500/month and spends >50% of their time on qualifying activities.

Phase 3: Economic Commitments

[ ] Local Business Spending (LBS): Meet the tiered annual spending requirement (see table below).

[ ] Capital Deployment Requirement (CDR): Commit to investing the lower of S$10 million or 10% of AUM in local Singaporean assets (SGX equities, local startups, or green bonds).

[ ] Philanthropy (Optional): If applying for the Philanthropy Tax Incentive Scheme (PTIS), appoint a philanthropy professional and increase LBS by S$200,000.

Phase 4: Formal Submission

[ ] MAS Tax Schemes Portal: Submit the application via the digital portal (live since 2025).

[ ] KYC/AML: Provide full UBO (Ultimate Beneficial Owner) transparency and AML policies.

II. 2026 Tiered Spending Requirements

The LBS is now strictly pegged to the AUM held in Designated Investments.

Assets Under Management (AUM in DI) | Min. Annual Local Business Spending (LBS) |

|---|---|

Below S$250 Million | S$200,000 |

S$250 Million – S$2 Billion | S$300,000 |

Above S$2 Billion | S$500,000 |

III. "Specified Income" & "Designated Investments" (2026 Update)

To enjoy the 0% tax rate, the income must be Specified Income (e.g., dividends, interest, gains) derived from Designated Investments.

Comparison of Key Investment Classes

Asset Class | 2026 Status | Notes for Family Offices |

Listed Equities/REITs | Included | Must be on MAS-approved exchanges for CDR credit. |

Digital Assets | Restricted | Generally excluded unless wrapped in specific qualifying fund structures. |

Physical Precious Metals | Enhanced | Now included (Gold/Silver/Platinum) up to 5% of portfolio (IPM status). |

Singapore Real Estate | Excluded | Income from SG immovable property is taxable; 13U only covers foreign real estate. |

Blended Finance | Bonus | Grants to local blended finance count as 2x spending toward your LBS. |

Private Equity/VC | Included | Includes shares in non-listed companies (except SG real estate holdcos). |

Pro-Tip: The "Closed-End" Election

If your fund has a fixed lifespan (e.g., a 10-year Private Equity style), you can now opt for the Closed-End Fund treatment. This allows you to meet LBS requirements on a cumulative basis rather than annually—perfect for the "harvesting" phase when AUM naturally declines as you exit investments.

Ready to Secure Your Family’s Legacy?

Singapore’s tax schemes offer a path to sustainable, tax-efficient wealth growth. For the latest updates on MAS circulars and filing requirements, consult with a Singapore-based tax expert to begin your application for Section 13U status.

Partnering with Bestar Singapore: Your 2026 Guide to Family Office Tax Incentives

Section 13U Fund Tax Scheme for Family Offices in Singapore

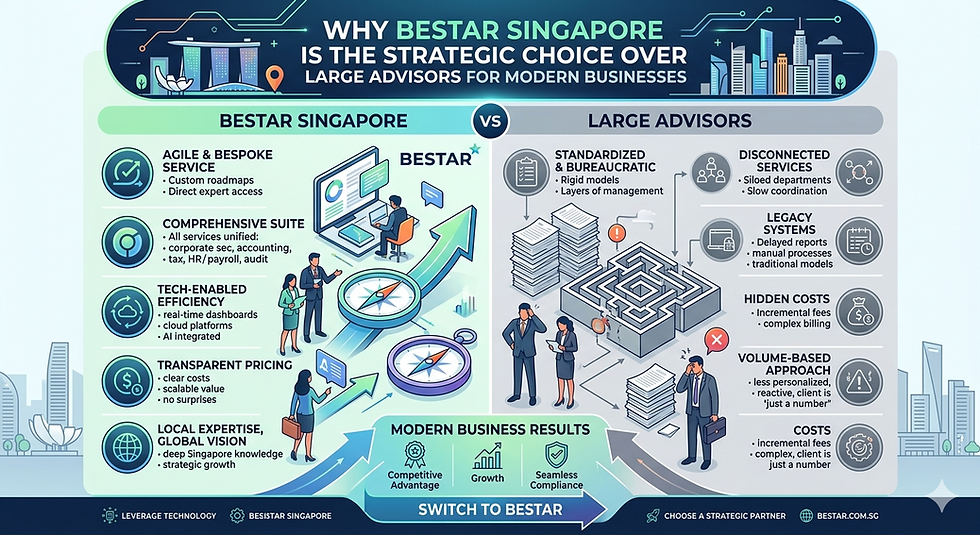

Navigating the 2026 regulatory landscape for wealth management requires more than just capital—it requires a partner who understands the intricate intersection of MAS compliance, tax optimization, and economic substance. Bestar Singapore is a premier, licensed tax and accounting consultancy specializing in end-to-end solutions for Section 13O and 13U tax incentive schemes. Whether you are a first-time applicant or looking to migrate an existing structure, Bestar’s 2026 framework ensures your family office remains a "Genuine Economic Entity" in the eyes of Singapore’s regulators.

Why Bestar Singapore is the Strategic Choice for SFOs

In an era where the Monetary Authority of Singapore (MAS) mandates rigorous screening reports and tiered spending audits, Bestar provides a one-stop ecosystem for high-net-worth families.

1. Expert Structuring & MAS Pre-Assessment

Bestar doesn’t just incorporate companies; we engineer legacy structures.

Tailored Entities: Advice on using Variable Capital Companies (VCCs) or Limited Partnerships to ring-fence assets.

AUM Verification: Ensuring your assets meet the S$20M (13O) or S$50M (13U) threshold specifically within the Designated Investments category—the new 2026 standard for eligibility.

2. Full-Spectrum Economic Substance Support

Substance is the cornerstone of 2026 tax residency. Bestar manages the logistics of your local presence:

Hiring Professionals: Managing the recruitment and Employment Pass (EP) applications for your required Investment Professionals (IPs).

Local Spending (LBS) Management: Bestar projects and tracks your tiered business spending to ensure you meet the minimum S$200,000 to S$500,000+ annual requirements without year-end "catch-up" risks.

3. Integrated Compliance & Philanthropy

With the 2026 focus on Philanthropy Tax Incentive Schemes (PTIS) and ESG mandates, Bestar helps families align their portfolios with the MAS "Finance for Good" initiative, potentially streamlining the approval process for 13U applicants.

Comparison: Bestar’s End-to-End Service Model

Service Area | Traditional Firm | Bestar Singapore (2026 Mode) |

Structuring | Basic Incorporation | VCC & Cross-border Trust Integration |

Tax Exemption | Standard Corporate Tax | S13O, S13U, & S13OA Specialization |

Immigration | Referral to agents | In-house Licensed EP/Work Pass Support |

Audit | Annual reporting only | 30-Day Audit KPI & Ongoing LBS Tracking |

Philanthropy | N/A | PTIS Advisory for 100% Tax Deductions |

Ready to formalize your family office in Asia’s premier financial hub? Bestar’s team, led by experts like Angela Tan (Private Tax & Family Office Leader), is available for 24/7 strategic consultation.

Head Office: 23 New Industrial Road, #04-08 Solstice Business Center, Singapore 536209

Phone/WhatsApp: +65 8836 4489

Email: admin@bestar-asia.com

Website: www.bestar-sg.com

Secure Your Family’s Global Future

The 2026 landscape for family offices is complex, but the rewards—0% tax on specified income and a foothold in Singapore—are unparalleled.

Comments