Compliance Guide: Section 201 of the Companies Act and Financial Reporting

- Roger Pay

- Apr 11

- 5 min read

Compliance Guide: Section 201 of the Companies Act and Financial Reporting

Navigating the Companies Act is a non-negotiable part of doing business in Singapore. Specifically, Section 201 outlines the legal responsibilities of company directors regarding financial transparency. Whether you are a startup founder or an experienced executive, understanding these requirements is crucial for maintaining your company’s "Good Standing" with ACRA.

Under Section 201 of the Companies Act, every director is legally obligated to present financial statements at the company's Annual General Meeting (AGM) that comply with prescribed accounting standards.

1. The Core Requirement: Compliance and Transparency

The primary goal of Section 201 is to ensure that shareholders and regulatory bodies have a "true and fair" view of the company’s financial health. Directors must ensure that financial statements:

Adhere to the Singapore Financial Reporting Standards (SFRS).

Are presented at the AGM within a specific timeframe (usually within 4 or 6 months after the financial year-end, depending on whether the company is listed).

2. Audited vs. Unaudited: Which Path for You?

The type of financial statements you must present depends entirely on your company's audit exemption status.

Scenario A: You are NOT Audit Exempted

If your company does not meet the "Small Company" or "Small Group" criteria, you are legally required to present audited financial statements under Section 201(1). This involves:

Appointing an independent public accountant to verify your accounts.

Presenting the auditor's report along with the financial statements.

Scenario B: You ARE Audit Exempted

If your company qualifies as a "Small Company," you can present a set of unaudited financial statements under Section 201(1).

Expert Tip: Even if you are audit-exempted, your financial statements must still be prepared in a format that complies with the Companies Act and SFRS. "Unaudited" does not mean "unstructured."

3. Quick Comparison: Reporting Requirements

Requirement | Audited Statements | Unaudited Statements |

Legal Basis | Section 201(1) | Section 201(1) |

Applicability | Non-exempt / Large Companies | Small Companies / Small Groups |

Verification | External Independent Auditor | Director-certified |

Filing with ACRA | Mandatory (XBRL where applicable) | Mandatory (XBRL where applicable) |

4. Key Takeaways for Directors

Failure to comply with Section 201 is a serious offense that can lead to fines or prosecution by ACRA. To ensure you stay compliant:

Determine Your Status: Regularly review if your company still qualifies for the audit exemption (the "Small Company" test requires meeting 2 out of 3 criteria regarding revenue, assets, and employees).

Keep Timely Records: Ensure your bookkeeping is up-to-date throughout the year to avoid the "year-end crunch."

Seek Professional Help: Engaging a qualified corporate secretary or accountant ensures your statements meet the prescribed accounting standards without the stress.

5. Frequently Asked Questions

What happens if I miss the AGM deadline?

If you cannot present financial statements within the timeline dictated by the Companies Act, you may need to apply for an Extension of Time (EOT) via ACRA's BizFile+ portal.

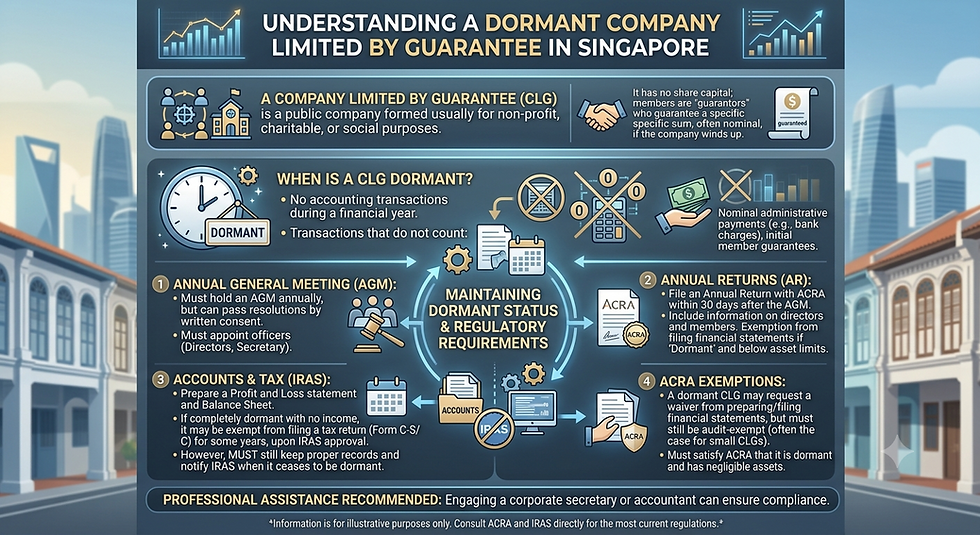

Do dormant companies need to present financial statements?

Yes. While dormant companies may be exempt from audit, directors are still required to prepare and present financial statements under Section 201 unless they meet specific exemption criteria for dormant relevant companies.

Are you unsure if your company currently meets the "Small Company" criteria for an audit exemption this year?

Seek Bestar Singapore Independent Auditor Help

Compliance Guide: Section 201 of the Companies Act and Financial Reporting

Choosing the right independent auditor in Singapore is more than just a compliance checkbox—it is a strategic move to safeguard your company’s reputation and financial integrity. As the 2026 reporting season approaches, businesses under the Singapore Companies Act must navigate evolving regulations with precision.

Whether your company is transitioning out of "Small Company" status or seeking to enhance stakeholder trust, Bestar provides the specialized audit and assurance framework necessary for modern corporate governance.

Why Your Business Needs an Independent Auditor

Under Section 201 of the Companies Act, directors of non-audit-exempt companies are legally required to present audited financial statements. However, the value of an independent auditor extends far beyond avoiding ACRA penalties.

1. Unbiased Financial Integrity

An independent auditor provides an objective "third-eye" perspective. Unlike internal teams, an external auditor has no financial stake in the business, ensuring that the Singapore Financial Reporting Standards (SFRS) are applied without conflict of interest.

2. Enhanced Stakeholder Trust

For companies looking to raise capital or secure bank loans, an audited report from a recognized firm like Bestar serves as a "seal of quality." It signals to investors and creditors that your financial data is reliable and transparent.

3. Risk Mitigation and Fraud Detection

Beyond checking numbers, modern auditing involves identifying operational leaks and internal control weaknesses. Bestar’s approach utilizes AI-driven audit tools to analyze 100% of ledger entries, catching anomalies that traditional manual sampling might miss.

Bestar’s Comprehensive Audit & Assurance Services

Bestar offers a "one-stop" solution that bridges the gap between daily bookkeeping and final statutory compliance.

Statutory Financial Audits: Tailored for companies that exceed the "Small Company" exemption thresholds (Revenue > S$10M, Assets>S$10M, or Employees > 50).

Internal Audit & Controls Review: Identifying bottlenecks in your financial workflows before they impact your bottom line.

Special Purpose Audits: Including grant audits, sales audits for MCST/retail, and due diligence for M&A.

XBRL Filing Support: Ensuring your financial data is mapped accurately to ACRA’s digital taxonomy.

Audit Exemption vs. Mandatory Audit (2026 Criteria)

To determine if you need to seek independent auditor help, evaluate your company against the "Small Company" test. You are exempt from audit if you meet at least two of the following three criteria for the past two consecutive financial years:

Criteria | Threshold for Exemption |

Total Annual Revenue | ≤ S$10 Million |

Total Assets | ≤ S$10 Million |

Number of Employees | ≤ 50 |

Note: If your company is part of a group, the entire group must qualify as a "Small Group" to maintain the exemption.

The Bestar Advantage: Seamless Transition

Switching auditors or preparing for your first statutory audit can be daunting. Bestar simplifies this through:

Digital Integration: 100% cloud-based workflows that reduce the audit cycle by up to 30%.

Pragmatic Solutions: We don't just find errors; we provide the infrastructure—from Chartered Secretaries to Tax Advisory—to fix them.

Fast Onboarding: For businesses looking to change providers, we offer a streamlined transition process to ensure no deadlines are missed.

Stay ahead of ACRA compliance and protect your corporate standing.

Does your company currently have the internal controls in place to facilitate a smooth year-end audit?

Streamline Your Compliance with Bestar

Don't let complex regulatory requirements slow down your business growth. Whether you need to determine your audit exemption status or require a full statutory audit, our team provides the precision and expertise needed to navigate the Singapore Companies Act with confidence.

Ensure your financial statements are compliant, transparent, and ready for filing.

Get Started Today:

Connect with a Specialist: Reach out for a tailored consultation on your corporate reporting needs.

Expert Note: To ensure maximum efficiency, we recommend conducting initial clarifications via email. This allows our specialists to review your company's structure and provide detailed, actionable guidance without an initial in-person meeting.

Comments