CLG Directors' Fees in Singapore

- Roger Pay

- 13 hours ago

- 6 min read

CLG Directors' Fees in Singapore

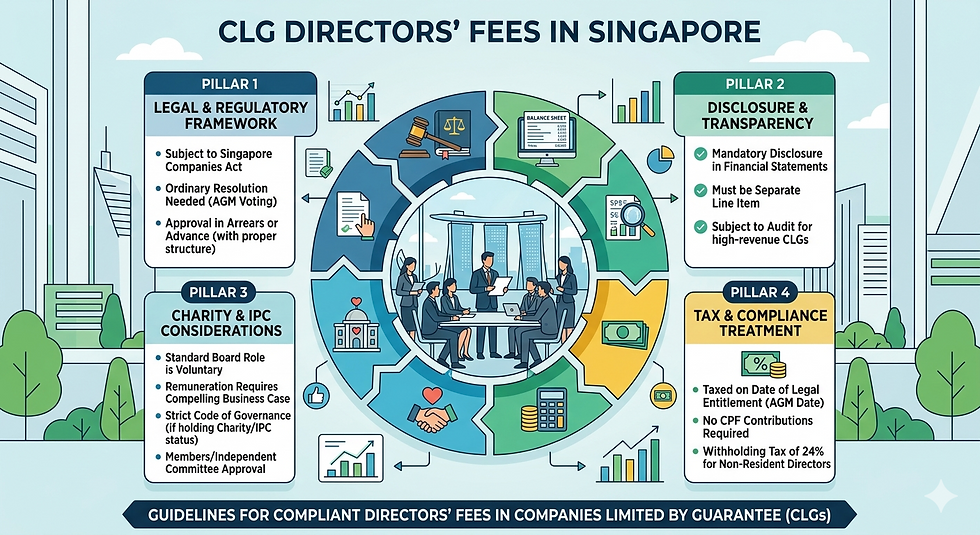

In Singapore, paying directors' fees in a Company Limited by Guarantee (CLG) requires balancing standard corporate law under the Companies Act with strict non-profit governance. Since CLGs are typically set up for charitable, non-profit, or public-interest purposes, the way these fees are structured, approved, and taxed involves a few unique considerations.

1. Corporate Governance & Approvals

Under the Singapore Companies Act, the core mechanics for approving directors' fees in a CLG mirror those of a normal private company, but with heightened sensitivity regarding its non-profit nature:

Ordinary Resolution Needed: Directors' fees cannot simply be decided or paid out by the board itself. They must be formally proposed by the board and voted on/approved by the members via an ordinary resolution, typically at the Annual General Meeting (AGM).

Approved in Arrears vs. Advance:

In Arrears: The most common route. Fees are approved at the AGM after the financial year has ended and the services have been fully rendered.

In Advance: To facilitate smoother cash flow, members can vote to approve a set pool or structure of fees for the upcoming year before the services are fully rendered.

Mandatory Disclosure: All approved directors' fees must be clearly and transparently disclosed as separate line items in the CLG’s audited or compiled financial statements.

2. The "Charity Status" Catch

While a basic CLG is allowed to pay reasonable fees to its governing board, the rules change drastically if the CLG holds or plans to apply for Registered Charity Status or Institution of a Public Character (IPC) status under the Commissioner of Charities:

Strict Charity Guidelines: Generally, charity board members and trustees serve voluntarily and should not receive directors' fees or remuneration for their role on the board.

If a charity wishes to remunerate a director, it must strictly comply with its own Constitution (which often explicitly prohibits or limits board remuneration) and the Code of Governance for Charities and IPCs. Any exception usually requires:

A compelling business case demonstrating that the payment is in the best interest of the charity.

Approval by an independent sub-committee or the general membership, where the interested director abstains completely from voting and discussion.

Clear disclosure in the annual report, often requiring exact branding of remuneration bands.

3. Tax & CPF Treatment (IRAS Rules)

When a CLG does pay directors' fees, the Inland Revenue Authority of Singapore (IRAS) applies specific rules based on tax residency and timing:

Feature, | Treatment for Tax & Compliance |

Taxable Year | Fees are taxed in the Year of Assessment (YA) matching the year the director becomes legally entitled to them. For fees approved in arrears, this is the exact date of the AGM where members voted approval. |

CPF Contributions | Not applicable. Central Provident Fund (CPF) contributions are not required on pure directors' fees, as they are not legally classified as employment salary. |

Withholding Tax | If the CLG appoints a non-resident director, any directors' fees paid to them are subject to a flat withholding tax rate of 24% (as of current tax frameworks). The CLG must withhold this amount and remit it directly to IRAS. |

Executive Directors vs. Non-Executive Directors

It is important to maintain a clear statutory distinction if a director also functions as an employee:

Pure Directors' Fees: Paid for governance/board duties. Approved at AGM. No CPF. Taxed on an entitlement basis.

Salaries/Bonuses: Paid if the director has an employment contract running the day-to-day operations (Executive Director). This is considered employment income, requires standard CPF contributions for residents, and is taxed on an accrual basis.

Navigating Growth: How Bestar Singapore Empowers Expanding Businesses

Scaling a business in a hyper-competitive hub like Singapore requires more than just automated software or basic, checkbox compliance. As operations grow more complex, small- to medium-sized enterprises (SMEs), multinational corporations (MNCs), and specialized entities face an intricate web of statutory auditing, tax optimization, ACRA compliance, and cross-border restructuring.

While digital-only corporate platforms offer quick, automated setups, they frequently fall short when a business encounters complex corporate actions, regulatory scrutiny, or a strategic transaction.

Bestar fills this gap as an ACRA-registered Public Accounting Corporation and comprehensive professional services firm. By combining cutting-edge AI financial technology with seasoned human advisory, Bestar provides the strategic oversight needed to turn compliance into a tool for corporate growth.

1. Statutory Audit & Assurance: Precision with a 30-Day Guarantee

An audit shouldn’t be a source of operational friction or an administrative bottleneck that stalls critical business decisions, funding rounds, or government grant applications.

Traditional auditing relies heavily on random sampling—reviewing a tiny percentage of transactions and extrapolating the results. Bestar modernizes this approach by integrating advanced data analytics and AI-driven audit co-pilots to perform full-population testing across your entire ledger. This identifies anomalies with extreme speed and precision.

30-Day Audit Guarantee: Bestar minimizes back-and-forth delays with a strict 30-day timeline for standard compliance cycles, ensuring statutory deadlines are met securely.

Direct Cloud Integration: The audit process connects seamlessly with major cloud accounting platforms like Xero and QuickBooks, alongside Singapore’s national e-invoicing standard, InvoiceNow. This direct synchronization reduces year-end document chasing by up to 30%.

Flawless XBRL Compilation: Financial statements are accurately converted into full-spectrum XBRL formatting to meet ACRA’s strict lodgment mandates without filing errors.

2. Integrated Corporate Secretarial & Governance Support

Under Section 171 of the Singapore Companies Act, every company must appoint a qualified corporate secretary within six months of incorporation. Rather than treating this role as a passive registry filler, Bestar operates an integrated business support model where corporate governance actively aligns with financial objectives.

The "All-Under-One-Roof" Advantage

When a corporate secretary works in isolation from the tax agent and auditor, communication gaps inevitably occur. At Bestar, corporate secretarial experts, tax advisors, and auditors sit under one roof. This guarantees that board resolutions, share capital adjustments, and statutory registers perfectly reflect your financial statements.

[Corporate Secretarial] <---> [Tax & GST Advisory] <---> [Statutory Audit]

^

|

(Perfect Alignment Under One Roof)

Specialist Governance Capabilities

Beyond routine maintenance of statutory registers (such as the Register of Registrable Controllers), Bestar provides dedicated support for complex corporate actions:

Specialized Entities: Managing compliance and structure for Companies Limited by Guarantee (CLGs), Single Family Offices (SFOs) navigating Section 13O/13U tax incentive schemes, and fund management structures.

Capital Restructuring: Drafting and executing complex resolutions for share capital reductions, currency conversions, and share buy-backs.

Global Expansion Support: Assisting foreign entities establishing a regional presence via branch offices, representative offices, and local nominee agent services.

3. Specialized M&A Advisory and Corporate Finance

Growth often accelerates through strategic consolidation. Navigating Mergers and Acquisitions (M&A), joint ventures, or divestitures requires specialized financial due diligence and absolute valuation accuracy.

Bestar's dedicated M&A advisory division works alongside business owners to protect value in and evaluate market opportunities:

Comprehensive Due Diligence: Uncovering hidden liabilities, analyzing financial positions, and assessing tax risks before executing agreements.

Meticulous Company Valuation: Utilizing a structured methodology to determine exact corporate worth, establishing a solid baseline for deal structuring and equity enhancement.

End-to-End Deal Execution: From evaluating initial proposals and structuring cross-border alliances to executing complex asset management strategies.

4. Comprehensive Tax, GST, and HR Consulting

Operating efficiently in Singapore means optimizing your tax exposure while maintaining a resilient, fully compliant workforce. Bestar’s multi-disciplinary team handles day-to-day corporate operations alongside long-term strategic planning.

Corporate Tax & GST Advisory: Structuring business transactions to maximize IRAS incentives, managing complex cross-border tax considerations, and handling local GST zero-rating queries.

Payroll & HR Outsourcing: Managing time-consuming administrative tasks, processing payroll, and ensuring statutory compliance with the Ministry of Manpower (MOM).

Visas & Immigration: Providing end-to-end management for Employment Pass (EP), Dependant Pass, and Permanent Residency (PR) applications, appeals, and renewals.

The Transition: Seamless Handover with Zero Downtime

Switching from a digital platform or an outdated provider to a high-touch professional firm does not require operational disruption. Bestar manages the entire cross-firm transition on a streamlined 30-day timeline:

Phase | Timeline | Key Actions & Deliverables |

1. Clearance & Discovery | Days 1–3 | Bestar secures professional clearance from your current provider and retrieves statutory registers with zero operational downtime. |

2. Data Sync & Mapping | Days 4–7 | Your accounting ledger (Xero, QuickBooks, or custom ERP) is securely linked to Bestar's automated analytics pipeline for pre-assessment. |

3. Testing & Verification | Days 8–21 | Chartered Accountants execute substantive testing, verifying data and addressing discrepancies via a single, dedicated interface. |

4. Sign-Off & Submission | Days 22–30 | The final independent auditor's report is issued, XBRL compilation is finalized, and filings are submitted to ACRA/IRAS. |

Strategic Takeaway: True financial governance requires actual advisory—not just automated dashboards. Bestar provides the scalable infrastructure of an elite firm combined with the agile, personal attention required by growing enterprises.

To evaluate your corporate compliance requirements:

Takes less than 2 minutes • 100% confidential under PDPA regulations • 1 business day response.

Comments